Find out if your lender is passing on the rate hike.

The Reserve Bank of Australia (RBA) has finally moved the needle on its monetary policy, ending the ultra-low-rate conditions by hiking the official cash rate for the first time since November 2010.

The central bank made a 25 basis point increase to the cash rate, bringing it to 0.35%.

The move follows the unexpected reading in inflation rates last week — according to the Australian Bureau of Statistics (ABS), the Consumer Price Index (CPI) rose 2.1% in the March 2022 quarter and 5.1% on an annual basis.

Meanwhile, the trimmed mean, which is the RBA’s preferred measure of underlying inflation, rose by 1.4% on a quarterly basis, the strongest increase since 2008.

In his statement, RBA governor Dr Philip Lowe confirmed there will be more rate rises ahead.

"The Board is committed to doing what is necessary to ensure that inflation in Australia returns to target over time. This will require a further lift in interest rates over the period ahead," Dr Lowe said.

"The Board will continue to closely monitor the incoming information and evolving balance of risks as it determines the timing and extent of future interest rate increases."

AMP Chief Economist Shane Oliver said the official cash rate could reach 2%.

"We expect the cash rate to rise to 1.5% by year-end and to 2% by mid next year. But the RBA will only raise rates as far as necessary to cool inflation and high household debt has likely made rate hikes more potent," he said.

"Rate hikes are unlikely to de-rail the economic recovery just yet as monetary policy is still very easy, but they will add to the slowdown in home prices, where we see average dwelling prices falling 10 to 15% into early 2024."

Will the rate hike affect mortgage repayments?

Bluestone Home Loans consultant economist Dr Andrew Wilson said this rate hike will not have a significant impact on existing borrowers.

“Existing mortgage holders and home buyers are currently well-positioned to absorb rate increases reflecting a strong, full employment economy with low unemployment rates and rising wages, record-level savings rates and the 3% repayment buffer imposed by banks on new borrowers,” he said.

CoreLogic research director Tim Lawless said this hike, however, will impact new borrowers.

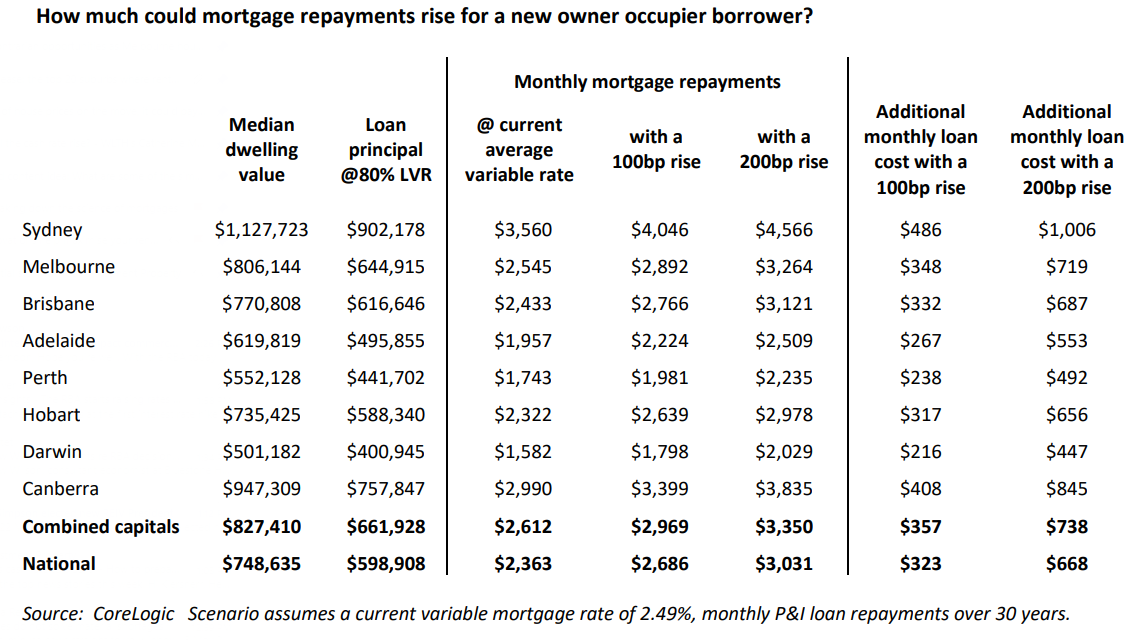

“Under a 100 basis point lift in variable mortgage rates, a new borrower in Sydney could be facing a rise in monthly mortgage costs of $486, while under a 200 basis point rise, monthly mortgage costs could be $1,005 higher than current levels,” he said.

The table below shows how much mortgage repayment could rise for new owner-occupier borrowers in each state under the 100bps and 200bps increases in variable rates:

Collections: Mortgage News Interest Rates RBA

Share