Dwelling prices continued to decline in August as the downturn becomes more widespread — at the same time, however, housing affordability improves.

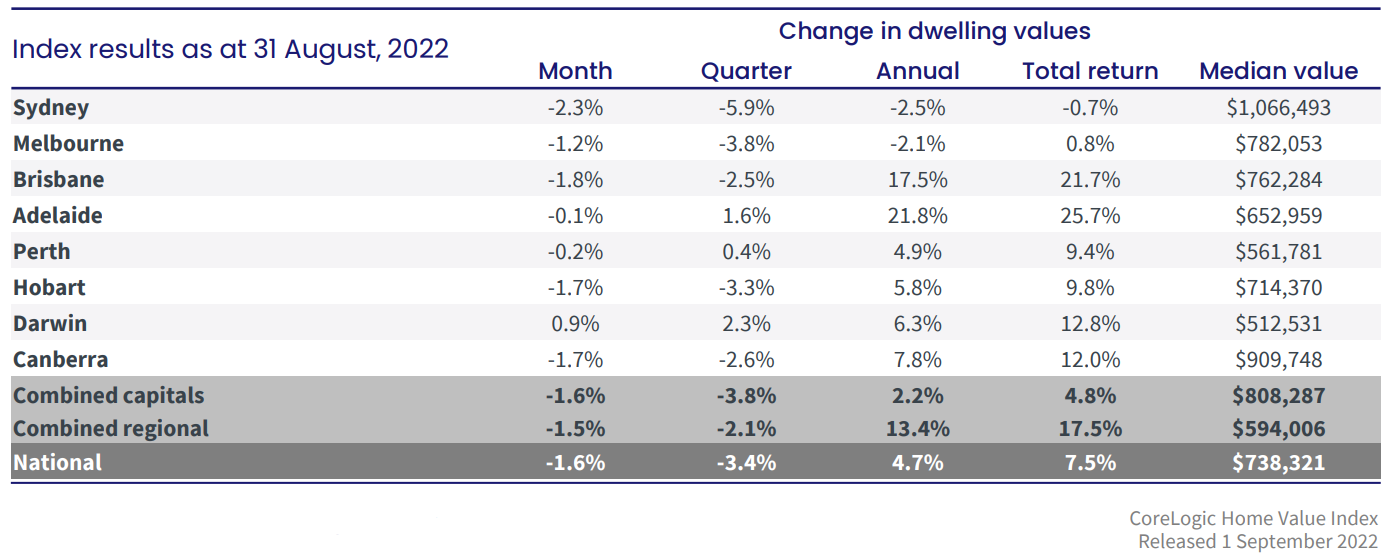

CoreLogic's Home Value Index in August showed a 1.6% decline in dwelling prices, driven by a 1.6% fall across capital cities and 1.5% decline in regional areas.

Every capital city apart from Darwin recorded a monthly fall in dwelling values over the month. Across regional markets, only regional South Australia reported an increase in dwelling values.

CoreLogic research director Tim Lawless said one of the most significant declines was in Brisbane, which has defied the slowdown over the past two years.

“It was only two months ago that the Brisbane housing market peaked after recording a 42.7% boom in values,” he said.

“Over the past two months, the market has reversed sharply with values down 1.8% in August after a 0.8% drop in July.”

Regional markets have also caught up with the overall downturn following months of stronger price growth.

Mr Lawless said the largest falls across regional markets emanated from the commutable lifestyle hubs where housing values had surged prior to the recent rate hikes.

“Over the past three months, values are down 8.0% across the Richmond-Tweed, 4.8% across the Southern Highlands-Shoalhaven market and 4.5% across Queensland’s Sunshine Coast,” he said.

With these recent declines, the annual trend in housing values appears to be rapidly levelling out.

In fact, the annual growth rate across capital cities fell to 2.2%, a significant fall from the peak of 21.3% recorded in November last year.

Housing affordability improves

A silver lining to the downturn in dwelling prices is the improvement in affordability.

According to ANZ CoreLogic Housing Affordability report for June 2022, the time needed for households on a median income to save a 20% deposit has fallen for the first time in almost two years across four capital cities.

In Sydney and Melbourne, there was a three-month reduction in the amount of time needed to save for the typical deposit requirement.

Affordability also improved in Canberra and Hobart, where the time needed to save a deposit declined by around one month.

Across Australia, however, the time it takes for households to achieve the typical deposit increased by less than a month compared to the previous quarter.

ANZ senior economist Felicity Emmett said one of the current challenges that could impact affordability are the likely rate hikes and increased cost of living.

“Households are in good shape to absorb further rate rises as people have been saving more; wages have increased, and many recent borrowers remain on low, fixed-rate mortgages,” she said.

Ms Emmet said borrower assessment on loans lodged recently have considered the potential rate rises.

“Mortgage serviceability assessment buffers mean that people who took out a new home loan over the past nine months should be able to absorb rate rises three percentage points higher than the variable rate at the time their mortgage was initiated.

“Also, mortgage serviceability may improve in 2024 — we expect the Reserve Bank of Australia to cut the cash rate by 50 basis points by the end of that year.”

—

Photo by abdul wasay's Images on Canva.

Collections: Mortgage News Property News

Share