Selling a home or real estate investment is no easy decision, and deciding to sell may be the easy part!

Knowing when to sell can be just as important – if not more so – than knowing the right time to buy. Selling a property is a significant financial and emotional decision with lasting consequences.

By understanding how (and when) the market cycles, tax implications, current conditions, and your future goals, you can turn a complex process into a strategic move that supports your long-term financial wellbeing.

When is the right time to sell a property?

Timing is everything in property investing, and can even play an important role when selling a primary place of residence. If you're wondering whether now's the right time to sell, ask yourself the following questions:

1. Does selling this property align with my long-term goals?

Ultimately, any decision to sell should be guided by your long-term goals – financial or otherwise. Will selling help you retire early? Improve your lifestyle? Free up capital for a passive income strategy? Or make it possible to buy your dream home?

If the sale is likely to set you back or derail your goals, it may be worth holding off – at least for now.

2. Do I believe the property's value will significantly increase?

Patience is a virtue, and owning property is often a long-term game. It can take years – sometimes decades – for a property's value to meaningfully increase. In some cases, it may never see much appreciation at all.

There are different factors to consider when selling your home or an investment property.

If an investment isn't expected to perform any time soon, the best day to sell may have been yesterday.

However, selling your home often means buying a new one, so consider what you expect to happen within the local market you're selling in and buying in. If they're different, take your expectations of both into account when making a decision. And if you're looking to upgrade, remember that while your property's value may be growing, the value of your dream home could be rising too.

3. Is the property costing me more to hold than I can reasonably afford?

Sometimes the decision to sell is purely financial. If the ongoing holding costs – mortgage repayments, maintenance, insurance, council rates – are outweighing the value you're getting in return (whether that's the security of owning your home or rental income), it might be time to let go. Though, it might be worth first considering if you can reduce such costs, perhaps by refinancing to a lower-rate mortgage. Here are some of the best offers on the market right now:

Lender Home Loan Interest Rate Comparison Rate* Monthly Repayment Repayment type Rate Type Offset Redraw Ongoing Fees Upfront Fees Max LVR Lump Sum Repayment Extra Repayments Split Loan Option Tags Features Link Compare Promoted Product Disclosure

Promoted

Disclosure

Promoted

Disclosure

Promoted

Disclosure

What's real estate 'selling season' and does it matter?

Once you've decided to sell, your next question is likely 'when should I sell?'

Spring is said to herald the 'selling season' for real estate in Australia, but some homes may be better suited to go to market at other times of year.

Buyers are said to be shaking off the winter doldrums and are more motivated to get out to home inspections. Meanwhile, homes are said to present better, with blooming gardens and increased natural light brightening up areas that may have looked a little dim in winter.

But Australia is a large continent. What applies to one market may not apply to all. Here are a few factors to consider if you're wondering when you should put your home up for sale.

Best month to sell a home across Australia

PropTrack analysts studied home price data over the ten years to 2023 finding November was the best month for Australian sellers, with prices typically 0.8% higher than the yearly average.

In monetary terms, such a discrepancy would mean someone selling a home worth around $800,000 would pocket an extra $6,000 more in November, compared to the average price achieved through the rest of a year.

Prices were also noticeably above average in the beginning of the year – 0.59% higher in February and 0.72% higher in March.

By contrast, the lowest seasonal prices were realised in winter – more than 0.9% below the average in both June and July.

Overall, PropTrack found spring time and the early months of the year were when homes sold for the most. However, the study noted there were differences in the data depending on which city or region you lived in.

In Sydney, Adelaide, and Hobart, the highest prices were typically achieved earlier in the year – in March for Sydney and Hobart and April for Adelaide.

Here's a capital city breakdown:

| Region | Best month to sell | Price difference (vs yearly average) | November (vs yearly average) |

|---|---|---|---|

| National | November | +0.8% | +0.8% |

| Sydney | March | +0.85% | +0.71% |

| Melbourne | October | +1.14% | +0.97% |

| Brisbane | October | +0.52% | +0.25% |

| Adelaide | April | +1.18% | +0.46% |

| Perth | November | +1.39% | +1.39% |

| Hobart | February | +1.46% | +1.16% |

| Darwin | March | +2.85% | -1.24% |

| ACT | November | +1.65% | +1.65% |

Source: PropTrack, 2023

The data shows all capital city markets, apart from Darwin, recorded above-average results in the so-called 'spring selling season' of October/November.

Some markets saw much more seasonal variation than others, with average prices considerably higher in their prime months compared to respective yearly averages.

This was most pronounced in Darwin, where prices were typically 2.85% higher in March. That's perhaps unsurprising, as the city's summer heat and seasonal rains are generally easing come March.

Seasonal factors also had a more pronounced effect on prices in Melbourne, Adelaide, Perth, and the ACT, where prices varied by well over 1% in peak selling seasons, whereas Brisbane tended to see very little seasonal variation compared to other cities.

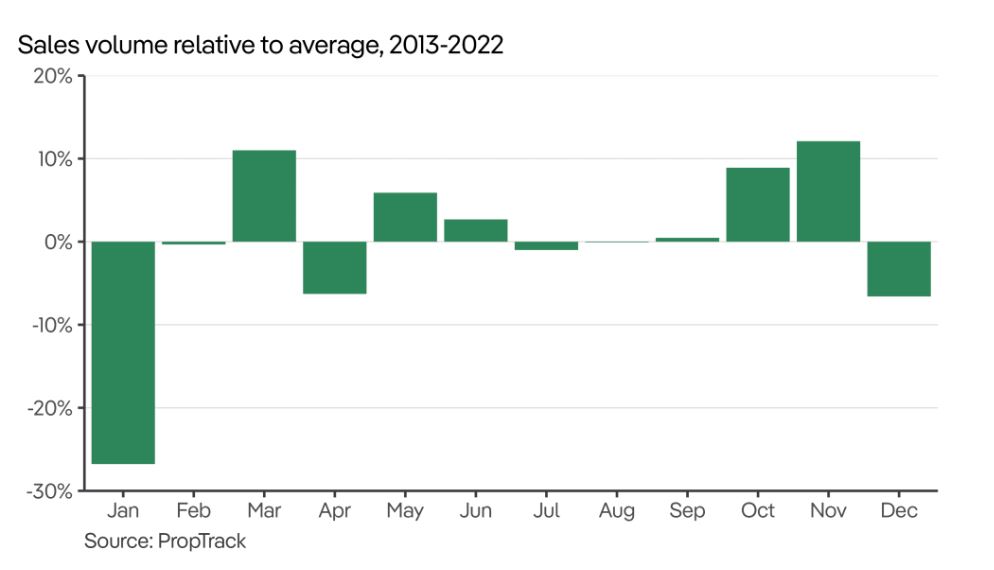

Sales activity around the nation

The study also ran the figures on sales volumes over the year, with data showing there can be noticeable differences in activity at different times.

Not surprisingly, holiday seasons – December-January and even April (Easter) – recorded significantly fewer sales than the yearly average.

Now that we know the best times of year for selling, according to research, let's look at what might lead you to sell your home.

How long should I own my home before selling it?

On average, Australians are staying in their homes for longer periods than they were in the previous decade. The average length of tenure for a house is now nine years, up from seven years in 2013.

Over the same period, unit owners are typically hanging onto their homes for eight years, up from six years.

These figures likely reflect the country's housing shortage, the higher cost of stamp duty (as home prices have risen), and simply less movement among Australians as the population ages and work arrangements become more flexible.

What to consider when selling a home or investment property

Selling a property isn't a set-and-forget task. There are numerous factors at play that can affect how smoothly the sale goes, how much you walk away with, and how it impacts your broader financial position. Strategic planning, smart timing, and a clear understanding of your obligations can make a significant difference to both your sale price and post-sale financial outcomes.

Here are some of the most important things to consider:

1. The condition and presentation of the property

First impressions count. Even if your property is an investment, it still needs to appeal to buyers – whether they're future landlords or owner-occupiers. That might mean making minor repairs, applying a fresh coat of paint, tidying the garden, or even staging the property for open homes.

Spending a little upfront to improve presentation can help you realise a higher sale price and reduce the time the property spends on the market.

2. Occupied vs vacant: which is better for selling?

Typically, remaining in your home during the sales campaign won't impact its appeal all that much. Though, you'll have to be comfortable with people walking through your space on a potentially regular basis. Thus, you'll probably want to keep the space presentable for the duration of the marketing campaign, which can be a pain.

If your investment property is one that's likely to continue being an investment rather than an owner-occupier home - it might be in a high-density apartment complex or a location popular with renters, for example – selling with quality tenants in place could be a good idea. A vacant home tends to attract more owner-occupier interest and can make the sales process more flexible. On the other hand, a tenant must legally be given notice before inspections, potentially slowing the sales process, while having tenants in place could deter homebuyers who want to move in immediately.

3. Market conditions and timing

Timing your sale with the market can make a big difference. A seller's market – characterised by high demand and low supply – can push prices up. A buyer's market, meanwhile, may require flexibility on price and longer selling periods.

Also consider:

- Local comparable sales

- Interest rate movements

- Seasonal trends (spring and early summer are often peak selling times)

Additionally, if your suburb has major upgrades in the pipeline – like a new school or train station – it could be worth holding off until works are completed to maximise value.

Speak with agents who specialise in selling property in your area for tailored insights.

4. Selling costs and agent commissions

There are various costs involved with selling a property, including:

- Real estate agent commission

- Advertising and marketing costs

- Legal or conveyancing fees

- Potential early exit fees if you have a fixed rate mortgage

- Capital Gains Tax (CGT)

Understanding these costs upfront ensures there are no nasty surprises and lets you work out how much you'll actually pocket after the sale.

Tax implications of selling an investment property

No matter what happens when you sell your investment property, there'll likely be a tax implication. If you make a profit, the Australian Taxation Office (ATO) will want a slice and if you make a loss, you might be able to reduce the tax you pay in the future.

If you sell for a profit – known as a capital gain – you'll likely face CGT. That means the profit you realise will be added onto your regular taxable income and you'll pay tax at the appropriate rate on the lot. Though, there are CGT discounts.

CGT discount

If you've owned the property for at least 12 months before selling, you're generally entitled to a 50% CGT discount as an individual taxpayer. This means only half of your capital gain is added to your taxable income.

The six-year rule (temporary absence rule)

If the property was originally your principal place of residence (PPOR) and you moved out and began renting it, you may still be eligible for a full CGT exemption under the six-year rule.

This rule allows you to treat the property as your main residence for CGT purposes for up to six years after you've moved out - even if you're earning rental income – as long as you don't own another property that you're treating as your main residence during that time.

Capital losses

If you sell the property for less than your cost base (original purchase price plus associated costs like legal fees, stamp duty, and capital improvements), you'll incur a capital loss. You can't claim this loss against your regular income, but you can carry it forward indefinitely to offset future capital gains.

For example, if you sell another asset down the track and make a capital gain, your carried-forward capital loss can reduce the amount of tax you need to pay on that gain.

Image by Steph Wilson on Unsplash

First published in September 2024

Collections: Selling your property Mortgage Statistics Post Collection

Share